During the planning phase of an assurance engagement, the internal audit engagement team identifies and evaluates the inherent fraud risks within the procurement function. What should be the engagement team’s next step?

According to the IIA Code of Ethics, which of the following is required with regard to communicating results?

An internal audit activity has to confirm the validity of the activities reported by a grantee that received a chantable contribution from the organization Which of the following methods would best help meet this objective?

Which of the following actions would an internal auditor perform primarily during a consulting engagement of a debt collections process?

An organization recently acquired a subsidiary in a new industry, and management asked the chief audit executive (CAE) to perform a comprehensive audit of the subsidiary prior to recommencing operations The CAE is unsure her team has the necessary skills and knowledge to accept the engagement According to IIAguidance, which of the following responses by the CAE would be most appropriate?

An internal auditor is tasked with evaluating the adequacy of the organization ' s inventory fraud controls. What is the most relevant information that the auditor can obtain from the documentation of cyclic counting for this purpose?

Which of the following best describes the manual audit procedure known as vouching?

When constructing a staffing schedule for the internal audit activity (IAA), which of the following criteria are most important for the chief audit executive to consider for the effective use of audit resources?

1. The competency and qualifications of the audit staff for specific assignments.

2. The effectiveness of IAA staff performance measures.

3. The number of training hours received by staff auditors compared to the budget.

4. The geographical dispersion of audit staff across the organization.

Which of the following is essential for ensuring that the internal audit activity ' s findings and recommendations receive adequate consideration?

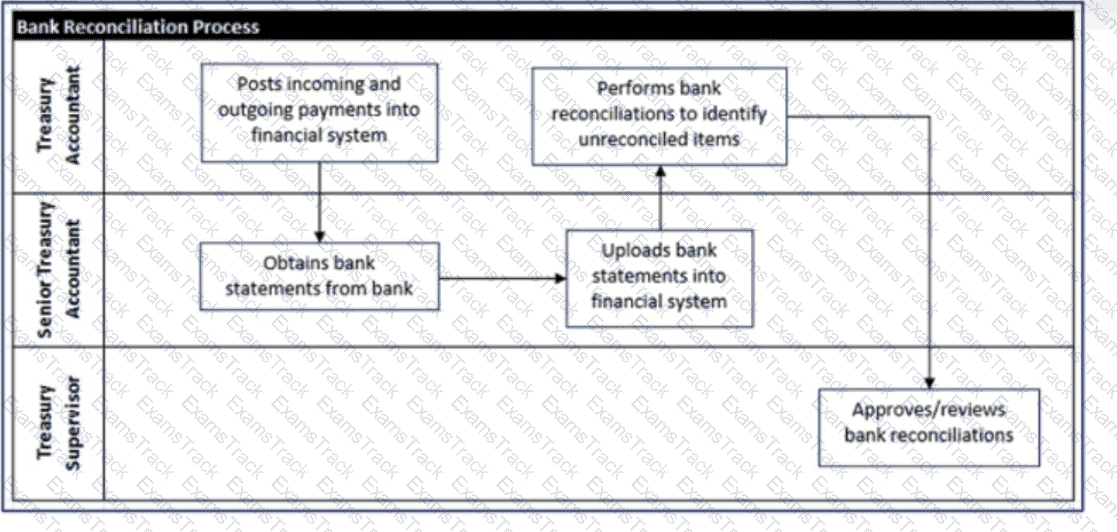

Below is a flowchart detailing an organization ' s bank reconciliation process. Which of the following conclusions can be drawn from the flowchart?

Which of the following would offer the strongest evidence to support the internal auditor ' s conclusion that a product is in stock, as stated in the accounting records?

|

PDF + Testing Engine

|

|---|

|

$49.5 |

|

Testing Engine

|

|---|

|

$37.5 |

|

PDF (Q&A)

|

|---|

|

$31.5 |

IIA Free Exams |

|---|

|

Copyright © 2026 Examstrack. All Rights Reserved

TESTED 12 Jul 2026